Be sure to set aside enough time for the conversation. If it’s your first meeting, you’ll want a half hour, at least.

Have your partner attend the meeting as it may be helpful for them to join.

Gather Your Important Documents

If possible, it can be helpful to have information on hand that can give the advisor a better sense of your situation and needs. Documents that could be useful include:

Existing insurance policies

Insurance coverage through work

Investments

Current debt (e.g. credit cards, mortgages, loans, etc.)

Whether you know exactly what protection you need or aren’t quite sure, there are some great introductory resources you can use to familiarize yourself before the call.

Your first call with an insurance advisor is for you to get to know each other so that you can feel more comfortable. You can use some of the questions below to gather some more information.

What services does the advisor provide?

What is your experience?

Who are your typical clients?

How will we work together?

What are your fees? How do you get paid?

Consider Your Goals

In your first meeting with an insurance advisor, they’ll want to get a sense of your needs and goals. It’s best to do some thinking ahead of time about your situation so you’re prepared.

How would my family be supported if I wasn’t around?

If I got sick or hurt and couldn’t work, how would I support myself and my family?

What is my current financial situation?

How will my family change in the future? Will it grow? Will my children become more independent? What then?

How much can I afford to spend, to protect what I have?

Commit to the Process and Know That We’re Here for You!

It’s important to realize that insurance planning is an ongoing process, not a simple transaction. It’s always a good idea to check-in annually to make sure you have enough coverage. And if you ever have a question, just ask! RBC Insurance advisors help people every day who are brand new to the world of insurance. Remember, we’re here to help you get it!

RBC Insurance advisors are here to help you learn and provide the information you need to feel confident in your decisions, without feeling obligated to purchase from us. We want to get to know you and your family so that we can best help you protect what’s important. With the help of this checklist, you’ll be prepared to get the most out of your next meeting with an advisor.

At RBC Insurance, we’re here to make sure you’re not alone in your quest for the right protection.

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

Meghan Parkinson bought her first car right after she graduated from college. It was a hefty purchase, but one that allowed her more independence to get to work, run errands and anything else that came up. At the time, Meghan (now 24) was feeling the post-grad financial burden in more ways than one. Student loans, rent and groceries were her biggest expenses, not to mention additional costs such as her cell phone plan and TV subscriptions.

“When I bought my car, I was pretty much drained money-wise,” she says, adding that she paid for the car outright, thanks to savings from various part-time jobs. Meghan says, while buying a car might feel like a glamorous purchase, the insurance that comes with it is anything but. Still, she knew it was important to find coverage that worked for her.

What the Experts Say

“I think I put in a lot more time researching car insurance than most people my age,” she said. “I researched insurance companies online and I talked to them on the phone. My main concern was which company was going to have the best deal for the most coverage options.”

Many young drivers are added to their parents’ car insurance policy as a “secondary” or “occasional” driver when they first get their license. Adam Mamdani, Vice President of Field Sales at RBC Insurance, says it’s helpful to begin building a track record as early as possible, and this is a good way to do so.

“If you are insured on your parents’ policy as an occasional driver, you can save money, you’ll gain experience and you’ll build a history,” he says. “But when you’re ready to buy your own car, your insurance will most likely look different because you don’t have the same years of experience that your parents had.”

It’s important to understand some of the factors that go into determining your car insurance premium, and your driving record is one of them. Mamdani says insurance companies will quote a price based on factors such as but not limited to your driving record, type of vehicle and gaps in insurance coverage.

Sometimes your gut instinct is to be removed from your parents’ policy when you’re away at school so that you don’t have to pitch in any extra money. It can save you more money in the long run by staying on and having continuous years of driving experience. You’ll appreciate this when it’s time for you to get your own policy.

Choosing the Right Coverage for You

Meghan opted for an insurance plan with “all-in” coverage, which includes collision and comprehensive coverage. Collision protects her car if it’s damaged in an accident, and comprehensive provides coverage against incidents such as theft, vandalism, weather damage and more. Her policy also includes accident forgiveness, which means her driving record will be protected if she had an at-fault accident.

The terminology alone can make car insurance shopping overwhelming, but Mamdani says a good way to start is by looking at mandatory coverages:

Liability — financial protection if you injure someone or damage property.

Property damage — covers you for damage to your car if you are not at fault in an accident.

Accident Benefits – provides coverage to you if you are injured in an accident or to your spouse, partner or dependent children if you pass away in an accident.

He says popular insurance add-ons include:

Collision coverage, which protects your vehicle if it’s damaged in an accident.

Comprehensive coverage provides coverage for your car in the event of theft, vandalism, fire, falling objects and other incidents.

Other optional add-ons could be coverage of loss, damage or theft of a non-owned vehicle, like a rental, and a waiver of depreciation, which guarantees that no depreciation will be applied to a vehicle that is less than two years old.

Regardless of which plan and add-ons you choose, Mamdani says the best way to save money is to have a clean driving record with no convictions or at-fault accidents, and to pay your bill on time, every time.

Some car insurance rules can vary by province so be sure to get advice from a Licensed Insurance Advisor.

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

Every 20 minutes, the family of a sick child arrives on the doorstep of one of Canada’s 15 Ronald McDonald Houses, according to the RMHC website. Since 1981, the organization has been offering lodging, meals and emotional support to families enduring pediatric hospitalizations.

For RMHC and other Canadian charities, adapting to the economic and societal shifts brought on by the COVID-19 pandemic has been challenging. Despite the challenges, many continue to adapt to what RMHC CEO Cathy Loblaw calls “a new world order.”

“We really had to stop, pause, think and figure out how to respond to the community needs, the hospital needs and the family needs simultaneously,” she says.

A 2020 survey by Imagine Canada measuring the impact of Coronavirus shows that 49 percent of organizations in the charity sector reported difficulty engaging volunteers, and 73 percent reported a drop in donations following the onset of the pandemic. Loblaw describes the arrival of COVID-19 as a time of rapid change and rapid growth at RMHC.

As Canadian charities continue to adapt to the changing world, so, too, can their supporters. There are several ways you can still contribute to your favorite charity, from a distance.

Fundraising and Public Safety

According to Imagine Canada, charities’ events-based fundraising revenue has dropped 72 percent in response to the pandemic.

“The largest part of our operating budget and funding comes from fundraising events,” says Loblaw, noting that such RMHC events have been cancelled in the interest of public safety.

While charity golf tournaments and events might be on hold, many other fundraising efforts have gone virtual. From auctions to black tie affairs, organizers and participants can stay connected online and contribute to a worthy cause.

Donating Where Possible

Volunteer-driven groups like RMHC may not be able to resume in-person programs anytime soon, but personal donations — even small contributions — can make a difference right now. Several charities accept financial gifts directly online, and if you’re an RBC cardholder you can choose to donate your rewards points to a group in need.

Creating Awareness Still Helps

Loblaw acknowledges that with many Canadians feeling the financial effects of the pandemic, monetary contributions might not be possible; creating awareness, however, may be. Sharing social campaigns, such as RMHC’s #givingtuesday initiative — a fundraising effort honoring the 387,000 families the organization has served since its inception — can be an effective, cost-free way to broaden the reach of your favorite organization.

Corporate Giving

Whether through leveraging marketing channels, encouraging employee donations, sponsoring or participating in a virtual event, or collecting wish-list items for local organizations, giving back together may strengthen your team and your community. Loblaw points to RMHC’s “deeply embedded partners like RBC Insurance” as critical sources of support.

We’re all adapting to new ways of doing things these days, including our charitable giving. If you are looking to support a charity or foundation that’s close to your heart, start by going to their website to find out how you can donate, or support through a new digital experience.

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

Did you know that about half of Canadians (49%) use a budget to manage their money? Creating a budget can help you control your spending, reduce debt, and prepare for the future. It gives you a clearer picture of where your money goes so you can make confident financial decisions.

In this article, we’ll walk you through simple steps to build a budget that fits your goals and lifestyle.

4 Steps to Create a Budget

Learn how to create your first budget with these four easy steps:

Step 1: Set a Clear Goal

Setting a budget can be beneficial, but creating one might not always feel compelling. It’s good to have a goal in mind when you create a budget so you’re more likely to stick to it.

Common budgeting goals and examples include:

Paying down debt

Managing money inflow and outflow so you don’t have to live paycheque to paycheque

Saving for a large purchase like a home or car

Saving for a trip

Increasing disposable income for savings or investments

Step 2: Calculate Your Income and Expenses

Calculate your monthly income and monthly expenses. In order to use more accurate numbers for this calculation, try to track everything you spend for one to two months. Remember to include things like your morning coffee, take out dinners and entertainment. This will give you a good idea of where your money goes. Tracking every single purchase might be difficult to do if this is new for you. See if your bank offers a service that tracks your spending, like the RBC NOMI app. Be extra mindful of the cash purchases you make and don’t forget to track them in a spreadsheet, a note in your phone or by using an app. There are apps available like Mint or Pocketguard, but do your research first to find one you’re comfortable using.

Once you have these results, compare what you make after taxes each month to what you spend.

If your expenditures are higher than your income, your first step is to reduce expenses where possible. This can be done in a number of ways — like cutting streaming services you don’t use often, curbing that excessive take out habit or something more significant like getting rid of a car.

Step 3: Divide Your Expenses

Divide costs into fixed, flexible, and future.

Fixed costs are the necessities (mortgage payments, utility bills, food)

Flexible costs are not necessary, but nice to haves (entertainment, gifts, memberships, and travel)

Future costs are savings, the things that may be needed one day (investments, an emergency fund, insurance)

A great way to divide these costs is by using the efficient 50-30-20 rule.

Set aside time each month to check-in. If you’re having trouble sticking to your budget, it might be time to try something new. You want your budget to be realistic and not the new mission impossible.

Find YOUR maintenance approach. Track spending with a spreadsheet, carry a set amount of cash instead of credit, or like 20 per cent of Canadians, try software or a mobile app to monitor money. Some helpful tools include Mint and Budget Planner by the FCAC. Whatever the approach, find a strategy that works for you.

TIP: If you are paid on a bi-weekly basis and set aside $50 each paycheque, you can save $1,300 in one year, before any interest.

Frequently Asked Questions (FAQs) about How to Budget

How to divide your budget

A practical way to divide your budget is by using the 50-30-20 rule. This means allocating 50% of your income to fixed expenses like housing, utilities, and transportation, 30% to flexible or personal spending such as entertainment or dining out, and 20% to savings, investments, or debt repayment. This method helps balance your needs, wants, and long-term goals while keeping your finances manageable.

What should your budget look like?

Your budget should include a detailed list of your income sources and all monthly expenses, divided into essential and non-essential categories. It should clearly show how much you earn, how much you spend, and how much you save each month. A good budget is realistic, easy to update, and tailored to your lifestyle so it can guide your day-to-day financial decisions.

How to make a monthly budget

To make a monthly budget, start by calculating your total monthly income after taxes. Then, track all your expenses for a month, including bills, groceries, transportation, and discretionary spending. Categorize each expense, compare it to your income, and adjust where necessary. Tools like RBC NOMI or Budget Planner by the FCAC can help automate tracking and identify spending patterns.

How to make a budget plan

A budget plan outlines how you’ll manage your money over time. Begin with a clear financial goal—such as paying off debt or saving for a down payment—then calculate your monthly income and expenses. Use those numbers to create spending limits for each category, allocate funds for savings, and set up automatic transfers or reminders to stay consistent.

How much should I spend on food per month?

As a general guideline, food expenses should make up about 10% to 15% of your monthly take-home income. This includes groceries, dining out, and snacks. Your exact amount may vary depending on your household size, dietary preferences, and location. Tracking your food spending for a few months can help you set a realistic target that fits your lifestyle.

What is a personal budget?

A personal budget is a plan that tracks your income, expenses, and savings so you can manage your money effectively. It helps you see where your money goes, avoid overspending, and reach financial goals like paying off debt or building an emergency fund. A personal budget can be created manually, in a spreadsheet, or with budgeting apps for convenience.

What should my budget be?

Your ideal budget depends on your income, expenses, and financial priorities. Start by covering essential costs like housing, food, and transportation, then allocate money for savings and discretionary spending. Many Canadians use the 50-30-20 rule as a starting point, but you can adjust the percentages based on your situation and goals.

RBC Life Insurance

Protect Your Loved Ones With Dependable Life Insurance.

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

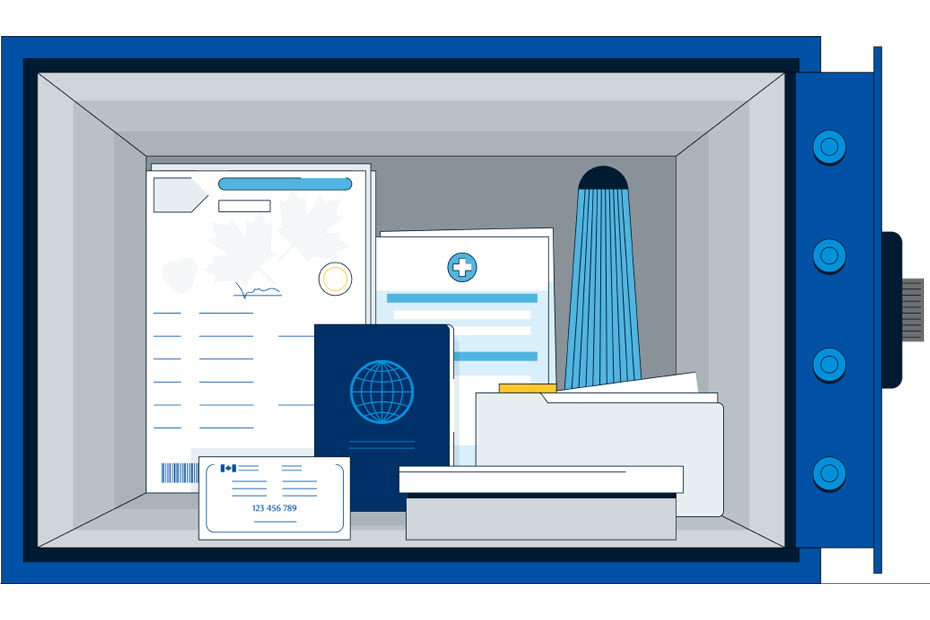

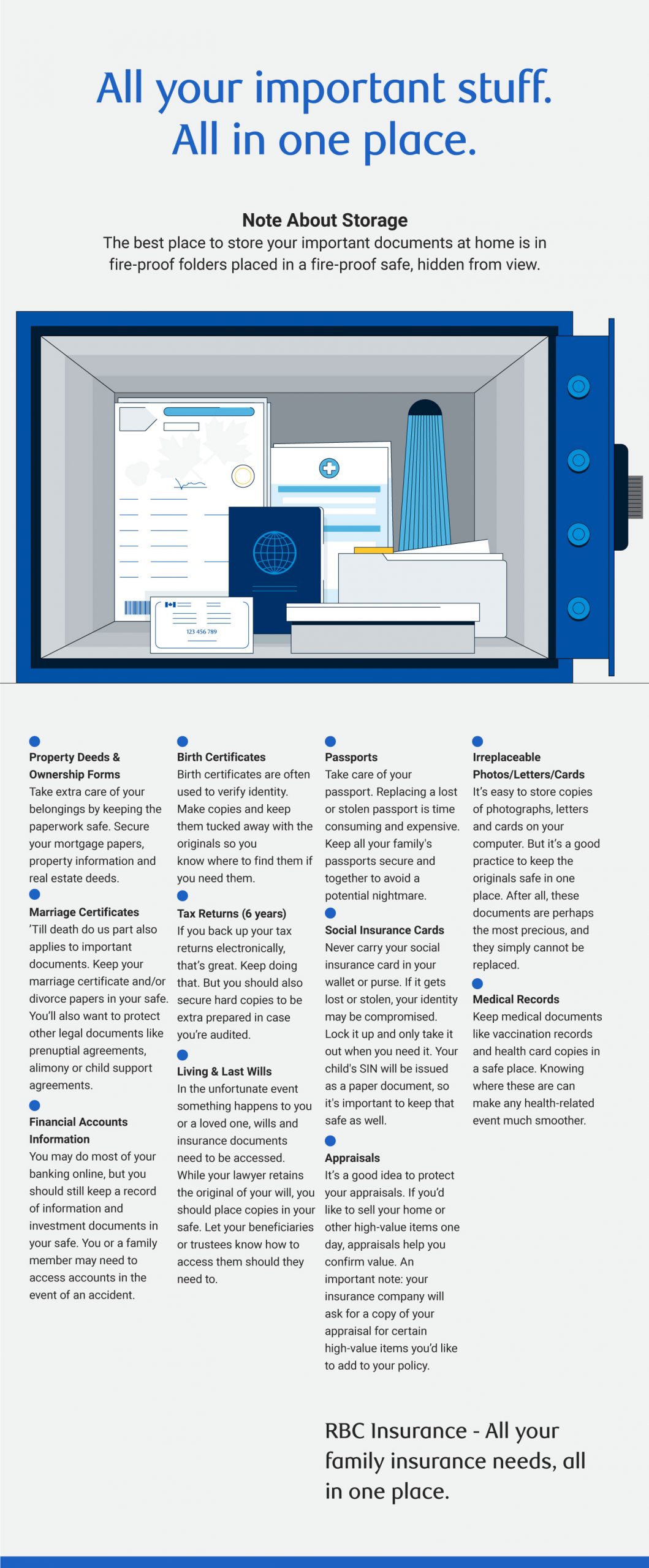

The best place to store your important documents at home is in fire-proof folders placed in a fire-proof safe, hidden from view.

Property Deeds & Ownership Forms

Take extra care of your belongings by keeping the paperwork safe. Secure your mortgage papers, property information and real estate deeds.

Marriage Certificates

“Till death do us part” also applies to important documents. Keep your marriage certificate and/or divorce papers in your safe. You’ll also want to protect other legal documents like prenuptial agreements, alimony or child support agreements.

Financial Accounts Information

You may do most of your banking online, but you should still keep a record of information and investment documents in your safe. You or a family member may need to access accounts in the event of an accident.

Birth Certificates

Birth certificates are often used to verify identity. Make copies and keep them tucked away with the originals so you know where to find them if you need them.

Tax Returns (6 years)

If you back up your tax returns electronically, that’s great. Keep doing that. But you should also secure hard copies to be extra prepared in case you’re audited.

Living and Last Wills

In the unfortunate event something happens to you or a loved one, wills and insurance documents need to be accessed. While your lawyer retains the original of your will, you should place copies in your safe. Let your beneficiaries or trustees know how to access them should they need to.

Passports

Take care of your passport. Replacing a lost or stolen passport is time consuming and expensive. Keep all your family’s passports secure and together to avoid a potential nightmare.

Social Insurance Cards

Never carry your social insurance card in your wallet or purse. If it gets lost or stolen, your identity may be compromised. Lock it up and only take it out when you need it. Your child’s SIN will be issued as a paper document, so it’s important to keep that safe as well.

Appraisals

It’s a good idea to protect your appraisals. If you’d like to sell your home or other high-value items one day, appraisals help you confirm value. An important note: your insurance company will ask for a copy of your appraisal for certain high-value items you’d like to add to your policy.

Irreplaceable Photos/Letters/Cards

It’s easy to store copies of photographs, letters and cards on your computer. But it’s a good practice to keep the originals safe in one place. After all, these documents are perhaps the most precious, and they simply cannot be replaced.

Medical Records

Keep medical documents like vaccination records and health card copies in a safe place. Knowing where these are can make any health-related event much smoother.

RBC Insurance — All your family insurance needs, all in one place.

Great Rates and Expert Advice on Home Insurance

Get a free online quote* for coverage to protect you, your property, and your belongings from the unexpected.

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

Life sometimes brings unexpected or unprecedented events that can be emotionally and mentally trying. A messy divorce, a serious illness, a devastating injury, the loss of a spouse or family member can all be traumatic in their own ways.

Watching someone you care for deal with loss may trigger feelings of helplessness if you’re unsure of what to say or do. Fortunately, there are number of ways to show your support and care for someone who’s going through a traumatic situation.

1. Be Available

Everyone reacts differently during hard times. The Canadian Mental Health Association suggests, “One of the most important things you can do is to simply be there for your loved one. Grief can feel overwhelming, but support and understanding can make a huge difference.”

Your friend may want to talk to you more often than usual or they may pull away and want to be alone. In either case, make sure they know that you’re there for them when and if they want to talk by phone, email, text or even video chat. The situation may feel awkward, but to support your friend, you need to be present, even if you can’t physically be there.

2. Listen Actively

As your friend talks through and processes their emotions, the best thing you can do is actively listen to what they are saying, according to Healthlink BC. Active listening means paying attention to the meaning behind their words, thinking about what they’ve said and responding in a way that shows you understand what they’re trying to communicate.

In some cases, your friend may not need or want you to respond right away or at all. You may have opinions, advice or thoughts to share, but hold on to them and just listen until your friend invites you to join the conversation.

3. Don’t Take Negative Reactions Personally

Traumatic events can trigger lots of emotions; your friend may be feeling angry, anxious, irritable, fearful, sad or emotionally numb. A difficult situation could make them feel helpless or like they’re not in control, which could lead them to lash out negatively towards friends and family.

If that happens, it’s important to remember that those reactions are natural, says the Mental Health Commission of Canada. “It is very important to reassure the person that stress reactions are normal responses to abnormal events.” While it may feel as though the reactions are directed at you, they’re not necessarily personal attacks. You can support your friend by letting them know that it’s okay to feel the way they do and encouraging them to feel their emotions in a healthy way.

4. Help Maintain Structure and Routine

Your friend may feel as if their world has been turned upside down and one way to help them is by reinforcing routines and habits. For instance if a friend is having a difficult time with self-isolation and maybe even the loss of a job, when the time is right you might encourage them to participate in activities or hobbies they enjoyed before like exercising, cooking, or learning something new like knitting or painting.

5. Be Mindful of Your Words

When someone is experiencing grief, there are some things they may not want to hear. As you talk to your friend, consider your words carefully. Avoid offering silver linings, trying to fix the situation or asking for more details about a situation than your friend is willing to share. If you’re not sure what to say, the safest course may be to say nothing at all and just continue listening.

6. Take Care of Yourself

Self-care may be as important for you as it is for your friend during a difficult time. You may want to be there for them 24/7, but you can’t be a good support system if you’re worn down or burned out, according to the Crisis and Trauma Resource Institute. Even professional caregivers may develop compassion fatigue, which is characterized by emotional, mental and physical exhaustion associated with caring for another person through a traumatic event. As you care for your friend, remember to take time for yourself regularly to recharge your batteries.

The mental, physical and emotional health of yourself and your loved ones is important.

RBC Disability Insurance

Help ensure your expenses are covered if you get sick or injured

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

Appointing a legal guardian for your children can offer some reassurance if something unexpected were to happen to you. Taking the time to research and thoroughly plan for this decision is important; this person should be someone you trust unequivocally, and someone you believe will raise your child with the same values and lifestyle that you would provide. In addition to drafting a will that names your chosen guardian, a life insurance policy may provide a financial cushion for your child, and a living trust is another option to help safeguard their future.

As you investigate the process of designating a legal guardian, here are the most important things to consider.

Choosing a Guardian

The primary issue to consider with legal guardianship is who will act as guardian.

Sounding out family members and friends can give you an idea of whom in your inner circle may be willing and able to accept a guardianship role if necessary. If you have more than one person you are considering and has expressed interest, these questions can be helpful in making a decision on guardianship:

Is this person someone whom you trust?

Does your child (or children) trust this person, and do they have a close relationship with them?

Is this person equipped mentally, emotionally and financially to handle the responsibility of raising a child full time?

Are they committed to continuing to raise the child the way you and your child are most comfortable with? For example, would the child be able to go to the same school, attend the same church, take part in the same activities, and be able to maintain their circle of friends?

Where would the child live? Would the legal guardian move into your home or would the child move into theirs?

Ultimately, who would be best for your child?

If you have two people who would be a great fit and want to be assigned guardianship, you might give them the choice of being a primary guardian or a successor guardian. The successor guardian can take over if the primary guardian isn’t able to continue caring for your child.

How Will My Child Be Supported Financially?

Planning with a guardian in mind is generally focused on providing the financial means to cover the expenses associated with raising children. Ask yourself:

What assets or resources do you have in place to pay for the child’s care? (This might include bank accounts, trust accounts, life insurance benefits, custodial accounts, an RESP or an RRSP.)

Who would have control over these assets? Would you want the legal guardian to have direct access to the money or would you rather have someone else in charge of financial decisions, such as your lawyer or financial advisor?

How do you want those assets to be used for your child’s care? For example, should a set amount be put aside to help with post-secondary costs?

How much will the legal guardian need to pay for your child’s care on a day-to-day basis and are the assets you have in place enough?

The assets you already have may give your legal guardian a good starting point for caring for your child financially, but look at your plan overall to see what else you may need.

Life insurance, for instance, may help. Your policy may be used to pay for funeral and burial expenses, but a life insurance benefit can also provide your child’s legal guardian with money to cover basic living expenses or pay for other costs, such as post-secondary education

When buying life insurance, there are three key questions to ask:

In choosing a beneficiary, remember that you can’t name your minor child directly. You could, however, name their legal guardian or a trustee if you’ve established a living trust on your child’s behalf. With a living trust, the trustee is bound to manage any assets transferred to the trust according to your specific wishes.

Review The Plan You Made for Your Child’s Guardian Regularly

A legal guardianship plan isn’t necessarily set in stone. Life changes or financial changes, such as having another child or inheriting a large amount of money, could require an update to your plan.

Even if you don’t experience those kinds of situations, it’s a good idea to check in with your guardianship plan at least once per year. Review your will and trust documents if you’ve established a trust. Check your life insurance coverage to make sure that it’s still sufficient to pay for your child’s care.

Finally, check in with the person you’ve chosen as a legal guardian to make sure they’re still comfortable with, and capable of, caring for your child. Ideally, they’ll never need to step into that role, but you want to be sure that they’re prepared to do so if necessary.

When it’s feasible, make some time to speak with your lawyer about a will and assigning a legal guardian and speak to an RBC Insurance advisor to discuss the best options for your family’s needs.

RBC Life Insurance

Protect Your Loved Ones With Dependable Life Insurance.

*Home and auto insurance products are distributed by RBC Insurance Agency Ltd. and underwritten by Aviva General Insurance Company. In Quebec, RBC Insurance Agency Ltd. Is registered as a damage insurance agency. As a result of government-run auto insurance plans, auto insurance is not available through RBC Insurance in Manitoba, Saskatchewan and British Columbia.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.